|

|

Post by code on Jun 4, 2022 16:17:59 GMT

You're welcome. PS: How's the treatment going? Well, I will drop you all a line. |

|

|

|

Post by duwayne on Jun 4, 2022 18:44:11 GMT

Why do you think the 2008 drop is a good guide to the present situation? That is a great question. I was not around during The Great Depression, but my father was. And I spent many an hour listening to tales from growing up in that period. No two economic downturns seem to replicate themselves exactly but as they say history tends to repeat itself. The roaring twenties culminated in a commodity price spike in 1929 followed by the collapse. 2008 was similar. The current situation is different but has some similarities. In 1929 and the following New Deal they did not do QE and supply liquidity to a struggling economy. They chose to let market forces sort it out. They dealt with their problems and chose not to pass the buck down to their kids and grandkids. In 2008 we went full fledged Keynesian. Programs like TARP, Cash For Clunkers and Quantitative Easing were the preferred strategy. Endless free money to banks and deficit spending were in vogue. When is the last time we had a balanced budget? The economy sucked up the free money and thrived for over a decade. Not much different than you and I paying our bills with a credit card. Lots of free cash if you put everything on a charge card. Well it is quite possible that the hens have come home to roost. Inflation is a problem. A real serious one. The Fed has to raise rates, raise rates and probably raise them some more as they start Quantitative Tightening. In short the one thing that has fueled are economy is now being removed. How will it respond? Anyones guess as we have never done it before. But I am old school. I don't subscribe to buying your way out of hard times with a credit card. Jamie Dimond and now John Waldron of Goldman Sachs have both come out with dire economic forecasts. I have never seen warnings like these in my life. They clearly know something. Here's what Jamie Dimond said in January of this year.

Jamie Dimon said the U.S. is headed for the best economic growth in decades. “We’re going to have the best growth we’ve ever had this year, I think since maybe sometime after the Great Depression,” Dimon told CNBC’s Bertha Coombs during the 40th Annual J.P. Morgan Healthcare Conference. “Next year will be pretty good too.”

Dimon said growth will come even as the Fed raises rates possibly more than investors expect."

Dimon clearly must have known something?

|

|

|

|

Post by missouriboy on Jun 4, 2022 19:36:51 GMT

That is a great question. I was not around during The Great Depression, but my father was. And I spent many an hour listening to tales from growing up in that period. No two economic downturns seem to replicate themselves exactly but as they say history tends to repeat itself. The roaring twenties culminated in a commodity price spike in 1929 followed by the collapse. 2008 was similar. The current situation is different but has some similarities. In 1929 and the following New Deal they did not do QE and supply liquidity to a struggling economy. They chose to let market forces sort it out. They dealt with their problems and chose not to pass the buck down to their kids and grandkids. In 2008 we went full fledged Keynesian. Programs like TARP, Cash For Clunkers and Quantitative Easing were the preferred strategy. Endless free money to banks and deficit spending were in vogue. When is the last time we had a balanced budget? The economy sucked up the free money and thrived for over a decade. Not much different than you and I paying our bills with a credit card. Lots of free cash if you put everything on a charge card. Well it is quite possible that the hens have come home to roost. Inflation is a problem. A real serious one. The Fed has to raise rates, raise rates and probably raise them some more as they start Quantitative Tightening. In short the one thing that has fueled are economy is now being removed. How will it respond? Anyones guess as we have never done it before. But I am old school. I don't subscribe to buying your way out of hard times with a credit card. Jamie Dimond and now John Waldron of Goldman Sachs have both come out with dire economic forecasts. I have never seen warnings like these in my life. They clearly know something. Here's what Jamie Dimond said in January of this year.

Jamie Dimon said the U.S. is headed for the best economic growth in decades. “We’re going to have the best growth we’ve ever had this year, I think since maybe sometime after the Great Depression,” Dimon told CNBC’s Bertha Coombs during the 40th Annual J.P. Morgan Healthcare Conference. “Next year will be pretty good too.”

Dimon said growth will come even as the Fed raises rates possibly more than investors expect."

Dimon clearly must have known something?

A whole bunch of people will be surprised.  Place your bets gentlemen.

|

|

|

|

Post by glennkoks on Jun 4, 2022 20:10:08 GMT

That is a great question. I was not around during The Great Depression, but my father was. And I spent many an hour listening to tales from growing up in that period. No two economic downturns seem to replicate themselves exactly but as they say history tends to repeat itself. The roaring twenties culminated in a commodity price spike in 1929 followed by the collapse. 2008 was similar. The current situation is different but has some similarities. In 1929 and the following New Deal they did not do QE and supply liquidity to a struggling economy. They chose to let market forces sort it out. They dealt with their problems and chose not to pass the buck down to their kids and grandkids. In 2008 we went full fledged Keynesian. Programs like TARP, Cash For Clunkers and Quantitative Easing were the preferred strategy. Endless free money to banks and deficit spending were in vogue. When is the last time we had a balanced budget? The economy sucked up the free money and thrived for over a decade. Not much different than you and I paying our bills with a credit card. Lots of free cash if you put everything on a charge card. Well it is quite possible that the hens have come home to roost. Inflation is a problem. A real serious one. The Fed has to raise rates, raise rates and probably raise them some more as they start Quantitative Tightening. In short the one thing that has fueled are economy is now being removed. How will it respond? Anyones guess as we have never done it before. But I am old school. I don't subscribe to buying your way out of hard times with a credit card. Jamie Dimond and now John Waldron of Goldman Sachs have both come out with dire economic forecasts. I have never seen warnings like these in my life. They clearly know something. Here's what Jamie Dimond said in January of this year.

Jamie Dimon said the U.S. is headed for the best economic growth in decades. “We’re going to have the best growth we’ve ever had this year, I think since maybe sometime after the Great Depression,” Dimon told CNBC’s Bertha Coombs during the 40th Annual J.P. Morgan Healthcare Conference. “Next year will be pretty good too.”

Dimon said growth will come even as the Fed raises rates possibly more than investors expect."

Dimon clearly must have known something?

Excellent points. But things have changed quickly, as they tend to do. In January the market showed no sign of weakness posting a new record, it's now down around 15% from that point. The biggest military conflict in Europe since WWII kicked off in late February. In the months since Dimon said this we found out that inflation was anything but transitory as it continued to increase the most in over 40 years. Last month India announced a ban on wheat exports. A lot has happened in the last six months. Legend has it JP Morgan (some say it was Joseph Kennedy) decided to get out of the market because a shoe shine boy was giving him hot stock picks. Before that epiphany one can assume that JP Morgan (or Mr. Kennedy) was in the market and heavily exposed. In the modern era Michael Burry started selling the housing market short in 2007. Before that correct forecast he was a very successful hedge fund manager. In business you have to change quick. I am not going to hold Dimon's January comments against him for changing directions. |

|

|

|

Post by ratty on Jun 4, 2022 23:09:59 GMT

[ Snip ] Excellent points. But things have changed quickly, as they tend to do. In January the market showed no sign of weakness posting a new record, it's now down around 15% from that point. The biggest military conflict in Europe since WWII kicked off in late February. In the months since Dimon said this we found out that inflation was anything but transitory as it continued to increase the most in over 40 years. Last month India announced a ban on wheat exports. A lot has happened in the last six months.Legend has it JP Morgan (some say it was Joseph Kennedy) decided to get out of the market because a shoe shine boy was giving him hot stock picks. Before that epiphany one can assume that JP Morgan (or Mr. Kennedy) was in the market and heavily exposed. In the modern era Michael Burry started selling the housing market short in 2007. Before that correct forecast he was a very successful hedge fund manager. In business you have to change quick. I am not going to hold Dimon's January comments against him for changing directions. Glenn, that's it in a nutshell. |

|

|

|

Post by code on Jun 5, 2022 16:40:54 GMT

[ Snip ] Excellent points. But things have changed quickly, as they tend to do. In January the market showed no sign of weakness posting a new record, it's now down around 15% from that point. The biggest military conflict in Europe since WWII kicked off in late February. In the months since Dimon said this we found out that inflation was anything but transitory as it continued to increase the most in over 40 years. Last month India announced a ban on wheat exports. A lot has happened in the last six months.Legend has it JP Morgan (some say it was Joseph Kennedy) decided to get out of the market because a shoe shine boy was giving him hot stock picks. Before that epiphany one can assume that JP Morgan (or Mr. Kennedy) was in the market and heavily exposed. In the modern era Michael Burry started selling the housing market short in 2007. Before that correct forecast he was a very successful hedge fund manager. In business you have to change quick. I am not going to hold Dimon's January comments against him for changing directions. Glenn, that's it in a nutshell. For sure, considering what he is now saying.

Dimon warned in May of “storm clouds” looming over the U.S. economy. He revised that assessment Wednesday at an annual conference sponsored by AllianceBernstein. “I said there were storm clouds, big storm clouds,” Dimon said. Now “it’s a hurricane.”

He added that even though the economy seems “fine” at the moment and “everyone thinks the Fed can handle this,” rough times are on their way.

|

|

|

|

Post by duwayne on Jun 5, 2022 17:29:00 GMT

[ Snip ] Excellent points. But things have changed quickly, as they tend to do. In January the market showed no sign of weakness posting a new record, it's now down around 15% from that point. The biggest military conflict in Europe since WWII kicked off in late February. In the months since Dimon said this we found out that inflation was anything but transitory as it continued to increase the most in over 40 years. Last month India announced a ban on wheat exports. A lot has happened in the last six months.Legend has it JP Morgan (some say it was Joseph Kennedy) decided to get out of the market because a shoe shine boy was giving him hot stock picks. Before that epiphany one can assume that JP Morgan (or Mr. Kennedy) was in the market and heavily exposed. In the modern era Michael Burry started selling the housing market short in 2007. Before that correct forecast he was a very successful hedge fund manager. In business you have to change quick. I am not going to hold Dimon's January comments against him for changing directions. Glenn, that's it in a nutshell. Ratty, are you saying that things might be a lot better 6 months from now? |

|

|

|

Post by ratty on Jun 5, 2022 20:22:17 GMT

Glenn, that's it in a nutshell. Ratty, are you saying that things might be a lot better 6 months from now? I'm really just agreeing that a lot can change in six months ... or a day for that matter. |

|

|

|

Post by glennkoks on Jun 5, 2022 21:25:25 GMT

Glenn, that's it in a nutshell. Ratty, are you saying that things might be a lot better 6 months from now? duwayne, I am interested in where you think things will be economically 6 months from now? I can't make money on the sidelines only lose less... I would love to hear a convincing argument as to why things will be better in 6 months from now and why I should jump back in. |

|

|

|

Post by duwayne on Jun 6, 2022 4:13:23 GMT

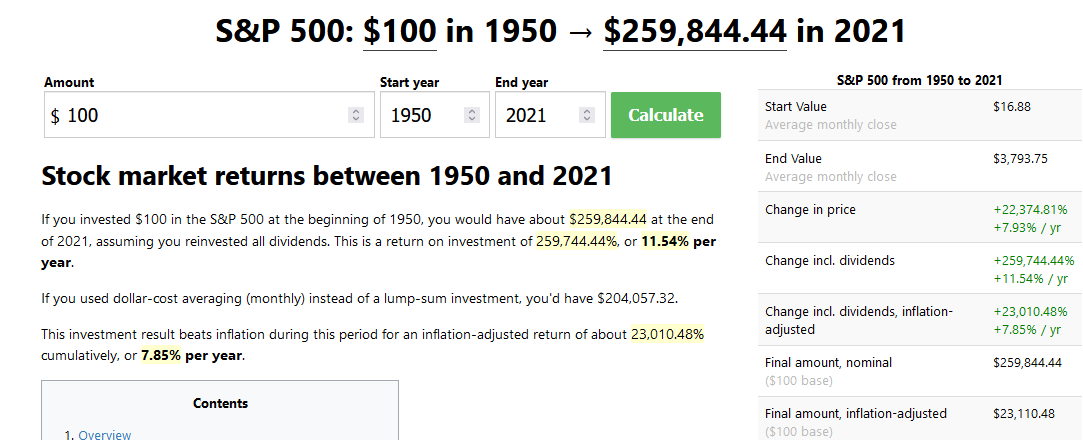

Ratty, are you saying that things might be a lot better 6 months from now? duwayne, I am interested in where you think things will be economically 6 months from now? I can't make money on the sidelines only lose less... I would love to hear a convincing argument as to why things will be better in 6 months from now and why I should jump back in. I’ll respond in another post to your question about the possible direction of the market, but first, I want to focus on your point that you can’t make money on the sidelines. The post below shows that if you had hypothetically invested $100 in an IRA-type account in S&P 500 index no-load funds in 1950, never bought or sold shares, and reinvested the dividends, it would have been worth almost $260,000 at the end of 2021.

This is a return on investment of 259,744.44%, or 11.54% per year.

I’m heavily biased toward a stock buy and hold philosophy for some portion of my savings.

If you go to the link below you can look at whatever period you choose. You’ll find that there hasn’t been a fall-off in performance in recent years.

There’s one other thing to note. If you look at the bottom right-hand corner of the figure above, you’ll see that after inflation, the value in 2021 would be only about $23,000. The message is if you don’t have your money in something that keeps up with inflation it’s going to lose its value.

My leaning is I don't have to be highly certain that the market is going up to be invested. I need to pretty certain that the market is going down if I decide to sit on the sidelines with all of my money.

|

|

|

|

Post by walnut on Jun 6, 2022 4:34:35 GMT

duwayne, I am interested in where you think things will be economically 6 months from now? I can't make money on the sidelines only lose less... I would love to hear a convincing argument as to why things will be better in 6 months from now and why I should jump back in. I’ll respond in another post to your question about the possible direction of the market, but first, I want to focus on your point that you can’t make money on the sidelines. The post below shows that if you had hypothetically invested $100 in an IRA-type account in S&P 500 index no-load funds in 1950, never bought or sold shares, and reinvested the dividends, it would have been worth almost $260,000 at the end of 2021.

This is a return on investment of 259,744.44%, or 11.54% per year.

I’m heavily biased toward a stock buy and hold philosophy for some portion of my savings.

If you go to the link below you can look at whatever period you choose. You’ll find that there hasn’t been a fall-off in performance in recent years.

There’s one other thing to note. If you look at the bottom right-hand corner of the figure above, you’ll see that after inflation, the value in 2021 would be only about $23,000. The message is if you don’t have your money in something that keeps up with inflation it’s going to lose its value.

My leaning is I don't have to be highly certain that the market is going up to be invested. I need to pretty certain that the market is going down if I decide to sit on the sidelines with all of my money.

But boy it helps if you are lucky enough to buy around the lows. |

|

|

|

Post by missouriboy on Jun 6, 2022 8:01:15 GMT

Ran across this interesting piece. How do historians measure historic values of economies at various points in time from bits and pieces of data? What do they have? Versus what do they miss? Some "ungenerous" sorts have argued that measures of modern wealth may also be contrivances of questionable worth.

|

|

|

|

Post by nonentropic on Jun 6, 2022 8:33:02 GMT

MB when I used to get the Economist before they became woke there was an admission of this even at a single time so they invented the concept Purchase price parity to account for value differences. Something like hookers in the third world are a fraction of the cost as they are in the west so there was a need for adjustment.

If you read Matt Ridley and his Rational Optimist the point of value inequality is lost in the overwhelming and sensational growth in average wealth.

We were all at school and university treated to the virtues of Maslow's hierarchy of needs and within that lives the problem you are talking of. That comes before such wonders as the I Phone and much more to further cloud the metrics that are applied.

But we live longer and have more stuff that is without dispute.

|

|

|

|

Post by walnut on Jun 6, 2022 12:25:11 GMT

MB when I used to get the Economist before they became woke there was an admission of this even at a single time so they invented the concept Purchase price parity to account for value differences. Something like hookers in the third world are a fraction of the cost as they are in the west so there was a need for adjustment. If you read Matt Ridley and his Rational Optimist the point of value inequality is lost in the overwhelming and sensational growth in average wealth. We were all at school and university treated to the virtues of Maslow's hierarchy of needs and within that lives the problem you are talking of. That comes before such wonders as the I Phone and much more to further cloud the metrics that are applied. But we live longer and have more stuff that is without dispute. "Purchase Price Parity" seems to not be immune from error or manipulation. I prefer to measure by "how much gold can you buy at the end of the year compared to others". That's the only parity I'm interested in. |

|

|

|

Post by glennkoks on Jun 6, 2022 12:28:57 GMT

duwayne, I am interested in where you think things will be economically 6 months from now? I can't make money on the sidelines only lose less... I would love to hear a convincing argument as to why things will be better in 6 months from now and why I should jump back in. I’ll respond in another post to your question about the possible direction of the market, but first, I want to focus on your point that you can’t make money on the sidelines. The post below shows that if you had hypothetically invested $100 in an IRA-type account in S&P 500 index no-load funds in 1950, never bought or sold shares, and reinvested the dividends, it would have been worth almost $260,000 at the end of 2021.

This is a return on investment of 259,744.44%, or 11.54% per year.

I’m heavily biased toward a stock buy and hold philosophy for some portion of my savings.

If you go to the link below you can look at whatever period you choose. You’ll find that there hasn’t been a fall-off in performance in recent years.

There’s one other thing to note. If you look at the bottom right-hand corner of the figure above, you’ll see that after inflation, the value in 2021 would be only about $23,000. The message is if you don’t have your money in something that keeps up with inflation it’s going to lose its value.

My leaning is I don't have to be highly certain that the market is going up to be invested. I need to pretty certain that the market is going down if I decide to sit on the sidelines with all of my money.

duwayne, Most of my life I have been heavily biased toward a buy and hold philosophy as well. Until recently I felt like I had enough time to ride out any downturns and just let the law of averages work. I just invested in S&P 500 index funds and forgot about it. My only attempt at timing the market came in 2020 during the Covid lockdowns and I admit it cost me some gains. My second attempt came in September of last year with the market around 34,000. My question to you would be what would the same portfolio you mentioned look like if you could have avoided the bulk of the 50% drop in 2008? I realize timing the top and bottom perfectly is nearly impossible but lets say you avoided 30% of the drop? I dare say that the portfolio scenario you mentioned would look much, much better. Personally I just can't wrap my head around the fundamentals of the economy over the last few years. From my perspective the market is overpriced. The Buffet Indicator is at 179%. Inflation is out of control and I feel is much higher in reality than the CPI is indicating. I think as the Fed turns off the free money valve and start to tighten the economy will start to sputter like and old internal combustion engine running out of fuel. Bottom line is this. I don't like the fundamentals and direction we appear to be headed. The market has been very good to me over the years. Missing out on potential growth is less of a concern to me than losing a large portion of what I have worked so hard to build. |

|

Place your bets gentlemen.

Place your bets gentlemen.